What Causes Sudden Credit Score Drops?

Written by A how To Company Contributor

What Causes Sudden Credit Score Drops?

Few financial surprises create panic faster than suddenly seeing your credit score drop.

One day your score looks healthy. Then suddenly it falls by 20, 40, or even 100 points seemingly out of nowhere.

Many people immediately assume identity theft or a major financial disaster happened.

Sometimes the explanation is serious. Other times the reason is surprisingly simple.

Credit scores can change quickly when new information is reported to the credit bureaus.

Quick Answer

The important thing to understand is that credit scores react to new data. When major changes appear on your credit report, scoring models may recalculate risk almost immediately.

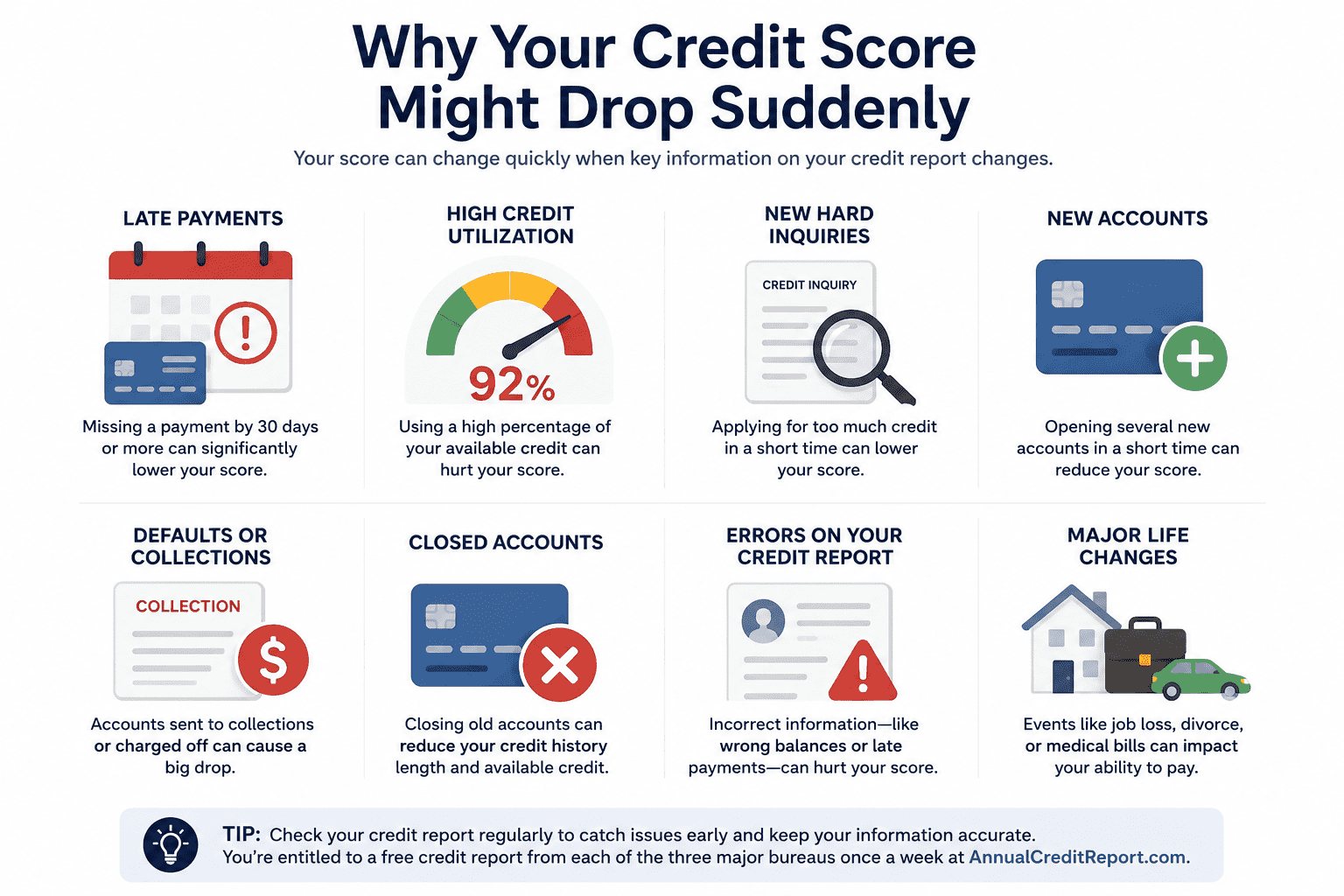

Why Sudden Credit Score Drops Happen

Credit scores are dynamic, meaning they constantly change as new information gets reported.

Your score is not permanently fixed.

Instead, it updates based on factors such as:

- Payment history

- Current balances

- Credit utilization

- New accounts

- Hard inquiries

- Collections and derogatory marks

Key Takeaway

Most sudden score drops happen because new information was recently reported to the credit bureaus.

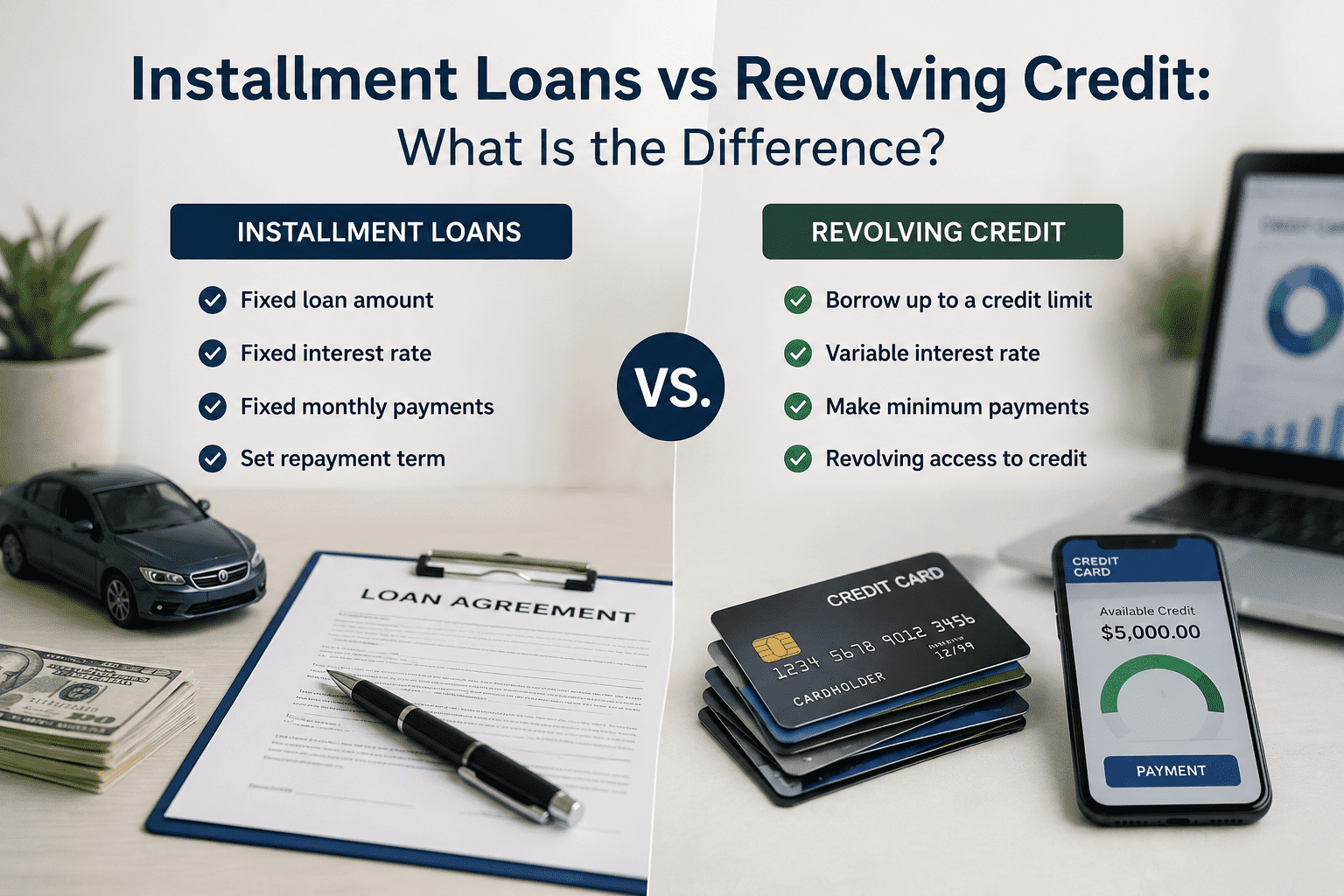

High Credit Utilization Is One of the Biggest Causes

Even if you plan to pay the balance off later, scoring models may still react negatively once the higher balance is reported.

According to the Consumer Financial Protection Bureau, high credit utilization may negatively affect credit scores because lenders may view it as increased borrowing risk.

Late Payments Can Cause Major Drops

Payment history is one of the most important parts of many credit scoring systems.

Even one missed payment can significantly damage a score.

The later the payment becomes, the more serious the impact may be.

- 30 day late payment

- 60 day late payment

- 90 day late payment

Each level may signal increasing financial risk to lenders.

Important Detail

People with previously strong credit scores sometimes experience larger drops from missed payments because the change represents a bigger shift in behavior.

Too Many Hard Inquiries and New Accounts

Applying for multiple credit accounts in a short period may also lower scores.

Hard inquiries occur when lenders check your credit during an application process.

While one inquiry may have only a small effect, several inquiries combined with new accounts may increase perceived lending risk.

No. Soft inquiries such as checking your own credit generally do not affect scores. Hard inquiries tied to credit applications may affect scores temporarily.

According to Experian, hard inquiries may remain on your credit report for up to two years, although their scoring impact is often shorter.

Closing Credit Cards Can Sometimes Hurt Scores

Many people assume paying off and closing a credit card is automatically good for their score.

However, closing accounts may:

- Reduce available credit

- Increase utilization percentages

- Affect average account age over time

This is why some people see unexpected score drops after closing older cards.

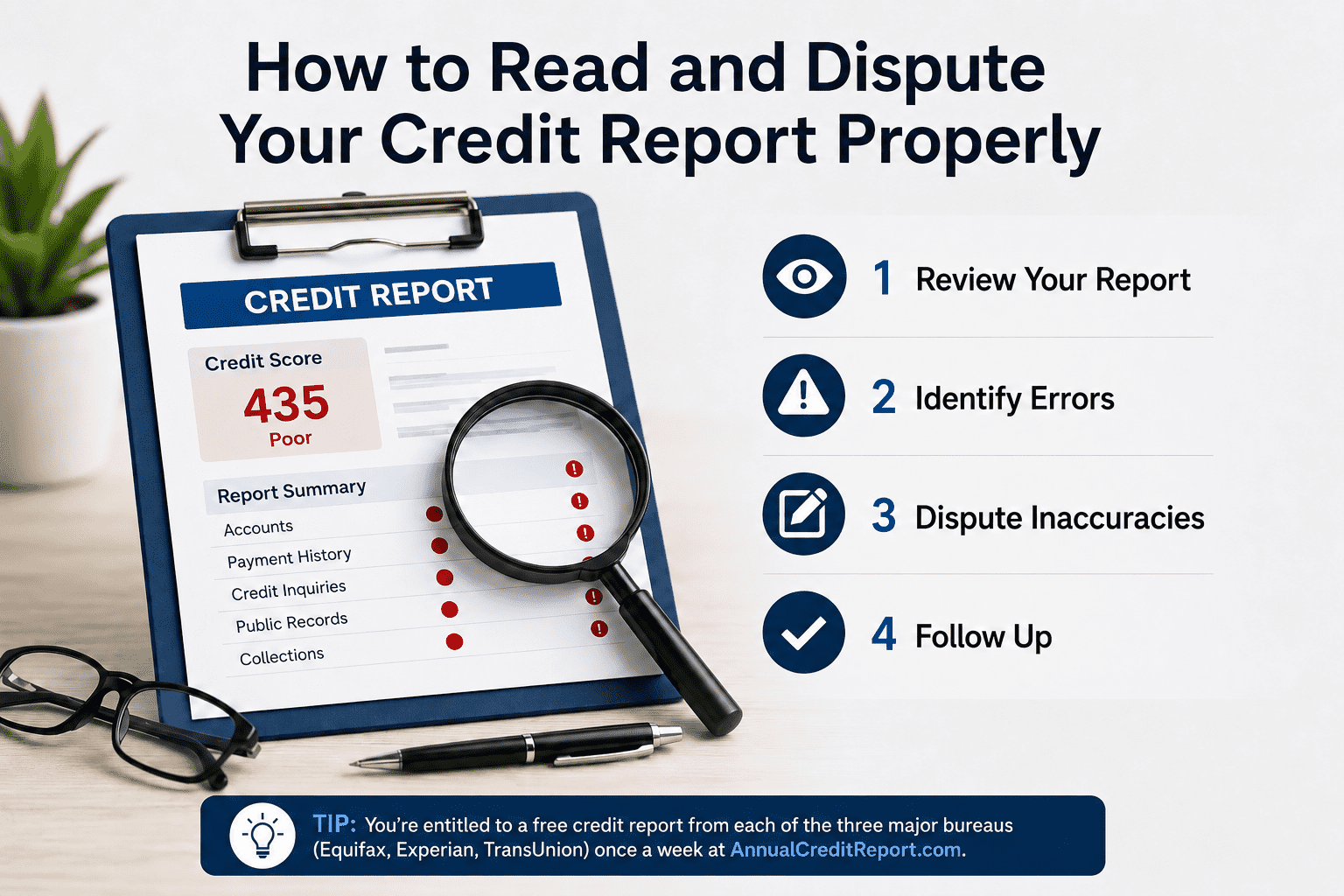

Credit Report Errors and Fraud Can Also Cause Drops

Not every score drop is caused by your own actions.

Sometimes the problem involves:

- Incorrect late payments

- Fraudulent accounts

- Identity theft

- Incorrect balances

- Collection reporting mistakes

According to the Federal Trade Commission, consumers should regularly review credit reports for potential inaccuracies and fraud.

Consumers can access reports through AnnualCreditReport.com, the federally authorized source for free annual credit reports.

Compare your most recent credit report with previous reports and look for newly reported balances, inquiries, missed payments, collections, or account changes.

Final Thoughts

Sudden credit score drops usually happen because scoring models are reacting to newly reported information.

In many cases, the biggest causes involve high utilization, missed payments, new accounts, or negative items appearing on a report.

The good news is that some drops can improve relatively quickly once balances decrease or errors are corrected.

Understanding why score changes happen can help reduce panic and make it easier to respond strategically instead of emotionally.

Monitoring your reports regularly and managing credit consistently are some of the best ways to prevent unexpected score surprises.