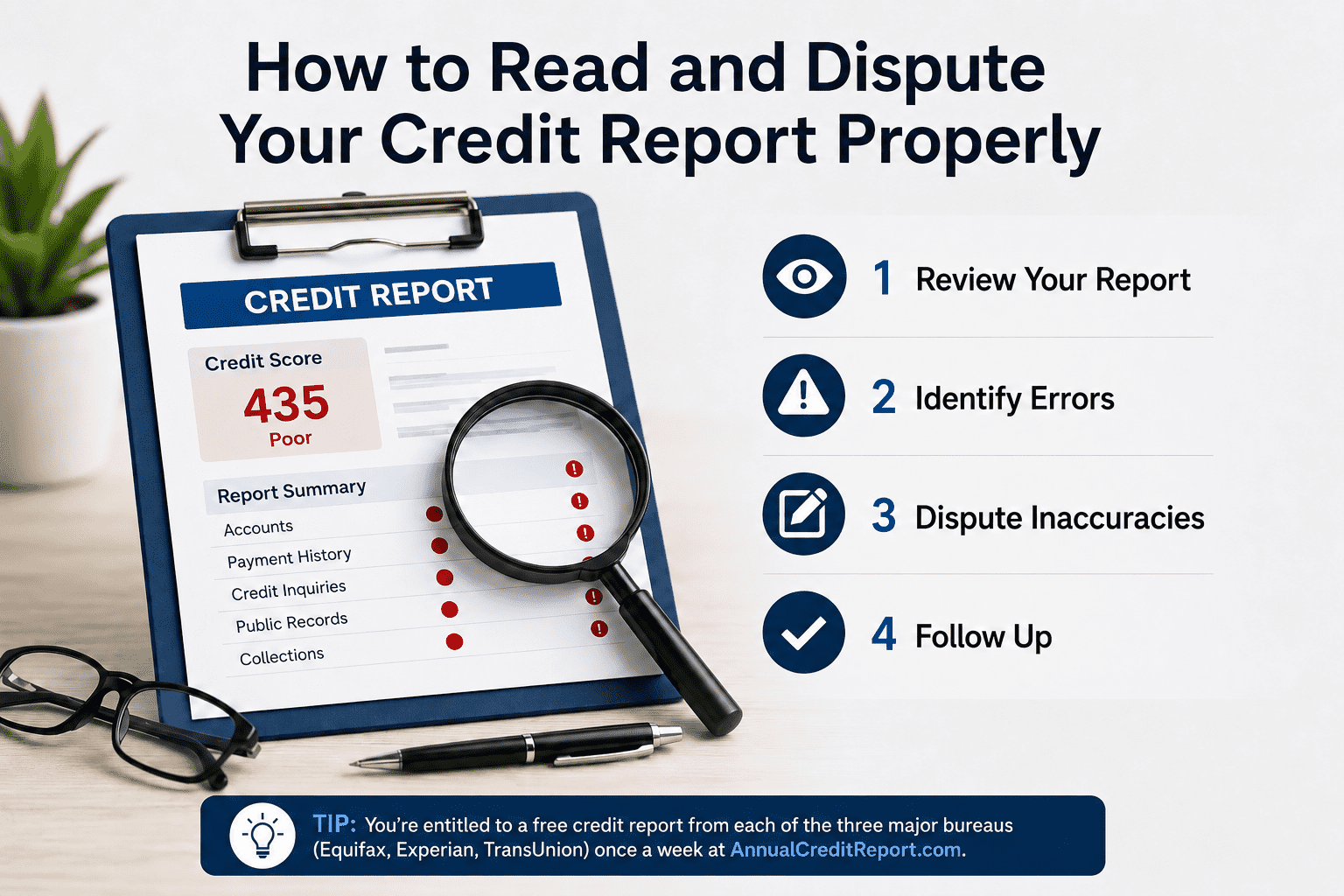

How to Read and Dispute Your Credit Report Properly

Written by A how To Company Contributor

How to Read and Dispute Your Credit Report Properly

Many people know their credit score, but far fewer actually understand how to read a full credit report.

That matters because credit reports contain the actual information lenders use to evaluate financial risk.

If inaccurate information appears on a report, it may affect approvals, interest rates, insurance pricing, apartment applications, and more.

Understanding how disputes work properly can help people correct legitimate errors while avoiding common mistakes that may hurt credibility.

Reading credit reports carefully and disputing errors strategically can help protect your financial profile.

Quick Answer

Credit report disputes allow consumers to challenge inaccurate information reported to the credit bureaus. Effective disputes require identifying legitimate errors, providing supporting documentation, and understanding when disputes are appropriate versus when they may backfire.

The goal should not be disputing everything randomly. The goal should be correcting inaccurate information accurately and strategically.

The Three Major Credit Bureaus

The three major nationwide credit bureaus in the United States are:

Experian collects and maintains consumer credit information reported by lenders, creditors, collection agencies, and other financial institutions.

Equifax maintains consumer credit files and provides credit reporting services used by lenders and businesses.

TransUnion organizes and maintains credit information that lenders may use during lending decisions.

According to the Consumer Financial Protection Bureau, these are the three nationwide credit reporting companies most consumers interact with.

Key Takeaway

Your credit reports may differ between bureaus because lenders do not always report the same information to all three companies.

How to Read a Full Credit Report

A full credit report contains much more information than just a credit score.

Important sections usually include:

- Personal information

- Current and previous addresses

- Employment information

- Credit accounts

- Payment history

- Credit limits and balances

- Collections

- Public records

- Credit inquiries

Consumers can access free reports through AnnualCreditReport.com, the federally authorized source for free credit reports.

How to Identify Inaccurate Information

Not every negative item is inaccurate.

This is extremely important because successful disputes are usually based on factual inaccuracies, not simply accounts someone dislikes.

Examples of potentially inaccurate information may include:

- Accounts that are not yours

- Incorrect late payments

- Wrong balances

- Duplicate accounts

- Incorrect dates

- Fraudulent accounts

- Accounts incorrectly reported as open or delinquent

A dispute is much stronger when you can clearly explain the exact error and provide documentation supporting your claim.

Disputing accurate information simply because it is negative may weaken credibility and often does not produce lasting results.

The Consumer Financial Protection Bureau lists identity errors, incorrect account information, and fraudulent accounts among common credit report problems consumers should monitor.

How Credit Report Disputes Work

When a consumer files a dispute, the credit bureau typically contacts the company that supplied the information and requests verification.

The furnisher must review the dispute and respond according to applicable reporting laws and procedures.

Consumers can generally dispute information:

- Online

- By mail

- Directly with the furnisher

According to the Consumer Financial Protection Bureau, consumers should explain what they believe is wrong and include copies of supporting documentation.

Strong Dispute Strategy

When Disputes Help vs When They Can Hurt

Legitimate disputes can absolutely help when inaccurate information exists.

However, excessive or inaccurate disputes can create problems.

- Identity theft accounts

- Incorrect late payments

- Wrong balances

- Duplicate reporting

- Incorrect account status

- Disputing accurate information repeatedly

- Submitting vague or unsupported claims

- Filing mass disputes without reviewing details

- Using generic dispute templates for everything

Some lenders may also become cautious when they see active disputes during underwriting because disputed accounts can temporarily complicate risk evaluation.

What Documentation Matters Most

Documentation can dramatically strengthen a dispute.

Helpful documentation may include:

- Bank statements

- Canceled checks

- Payment confirmations

- Settlement letters

- Identity theft reports

- Account statements

- Police reports if applicable

- Official creditor correspondence

Important Detail

According to the CFPB, consumers should include copies rather than original documents when submitting disputes.

You can learn more from the Consumer Financial Protection Bureau.

Final Thoughts

Learning how to read and dispute a credit report properly is one of the most valuable financial skills consumers can develop.

Effective disputes focus on legitimate inaccuracies, organized evidence, and clear communication.

Randomly disputing accurate information is usually far less effective than carefully reviewing reports and targeting specific errors with documentation.

The strongest credit dispute strategy is accuracy, organization, documentation, and patience.