Why Credit Scores Vary Between Credit Bureaus

Written by A how To Company Contributor

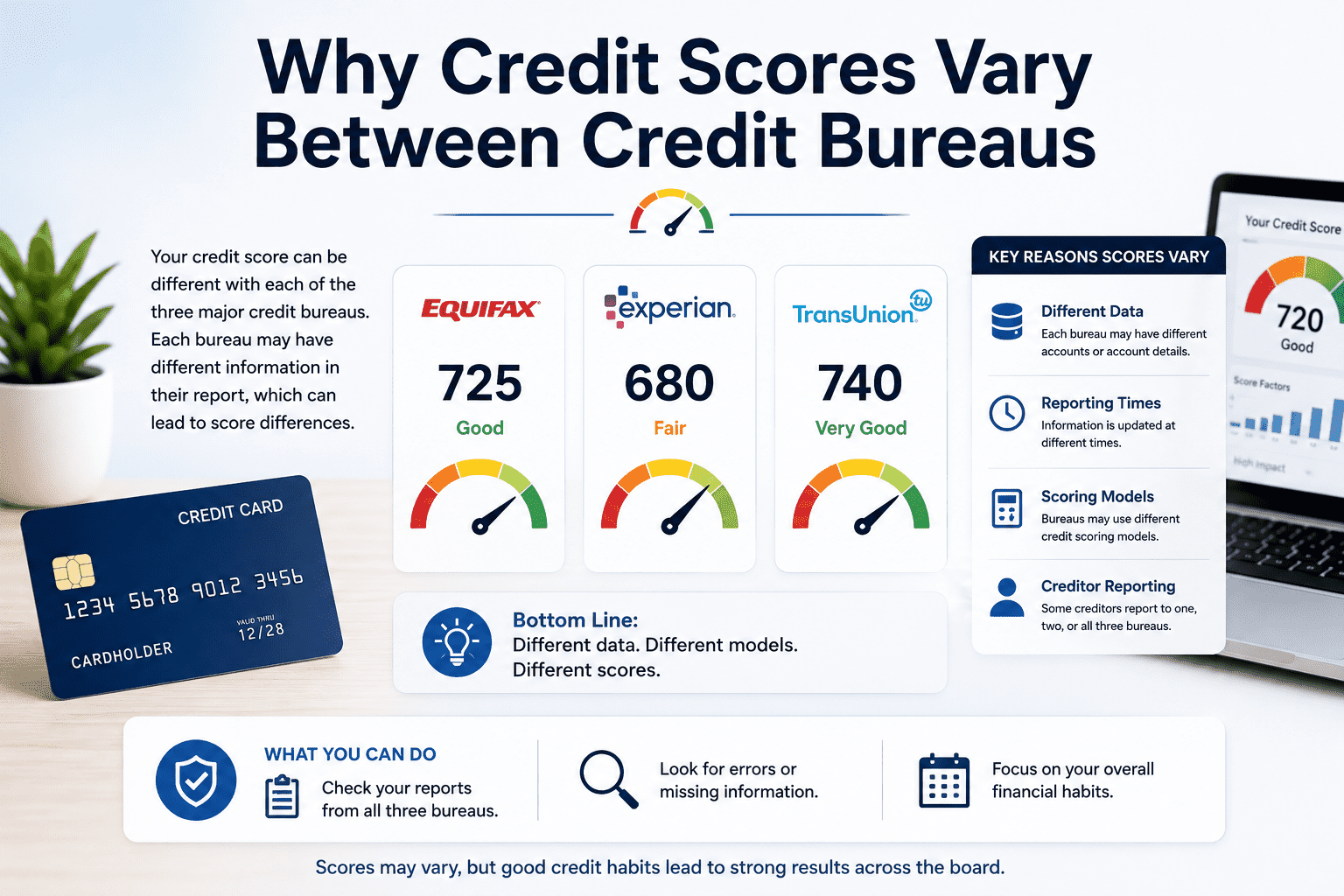

Why Credit Scores Vary Between Credit Bureaus

Many people check their credit and feel confused when Experian, Equifax, and TransUnion do not show the exact same score.

One bureau might show 721. Another might show 738. Another might show 704.

That can feel alarming, especially if you are preparing for a loan, apartment application, car purchase, or mortgage approval.

The good news is that score differences between bureaus are extremely common.

Credit scores can vary between bureaus because each bureau may have different information, reporting dates, and scoring models.

Quick Answer

In other words, a different score does not automatically mean something is wrong.

But it does mean you should understand why those differences happen.

The Three Major Credit Bureaus

In the United States, the three major nationwide credit reporting companies are Experian, Equifax, and TransUnion.

According to the Consumer Financial Protection Bureau, these companies are the three nationwide providers of consumer credit reports.

TransUnion gathers and organizes credit information in a similar way, but its report may not always contain the exact same data found at Experian or Equifax.

Key Takeaway

Reason 1: Not Every Lender Reports to Every Bureau

This is one of the biggest reasons credit scores vary between bureaus.

A credit card company might report your account to all three bureaus. Another lender might report only to Experian and TransUnion. A smaller lender may report to only one bureau.

According to Equifax, not all lenders and creditors report to all three nationwide credit bureaus.

That means one bureau may have an account listed while another bureau does not.

Reason 2: Information Updates at Different Times

Even when a lender reports to all three bureaus, the updates may not appear on the same day.

One bureau may update your new balance today. Another bureau may update it several days later.

This can make your scores temporarily different, especially after:

- Paying down a credit card

- Making a large purchase

- Opening a new account

- Closing an account

- Having a new inquiry reported

Important Reality Check

Timing matters. Two scores pulled on different days may differ simply because one bureau has newer information than another.

myFICO explains that comparing scores pulled at different times can be misleading because credit data and scoring factors can change over time.

You can learn more from myFICO.

Reason 3: Different Scoring Models May Be Used

A score from one bureau may not match another because the same scoring model was not used.

There are many scoring models, including different versions of FICO Scores and VantageScores.

The Consumer Financial Protection Bureau explains that different companies use different score ranges and scoring approaches.

This means a score from a credit card app, mortgage lender, auto lender, or free credit monitoring platform may not be calculated the same way.

Reason 4: Errors or Missing Information Can Create Bigger Differences

Sometimes score differences are normal.

Other times, they may point to an error.

Common credit report errors include:

- Accounts that do not belong to you

- Incorrect late payments

- Wrong balances

- Duplicate accounts

- Identity mix ups

- Fraudulent accounts

The Consumer Financial Protection Bureau lists several common credit report errors consumers should watch for, including identity errors, incorrect account information, and accounts resulting from identity theft.

When to Pay Closer Attention

If one bureau shows a much lower score than the others, review that credit report carefully. A large difference may indicate missing positive information, inaccurate negative information, or fraud.

What Should You Do If Your Scores Are Different?

First, do not panic.

Small differences are normal.

But you should still review your reports carefully, especially before applying for major credit.

- Check all three credit reports

- Compare account balances

- Look for missing accounts

- Review late payments carefully

- Check for accounts you do not recognize

- Dispute inaccurate information

The Federal Trade Commission recommends reviewing credit reports to check for mistakes and signs of identity theft.

Consumers can access free credit reports through AnnualCreditReport.com, the federally authorized source for free credit reports.

Final Thoughts

Credit scores vary between bureaus because credit reporting is not perfectly identical across Experian, Equifax, and TransUnion.

Lenders may report to different bureaus, updates may happen at different times, and scoring models may calculate risk differently.

A small difference between scores is usually normal. A major difference deserves closer review.

The smartest approach is to monitor all three reports, correct errors quickly, and focus on the habits that improve your credit across every bureau.