How Hard Inquiries and Soft Inquiries Work

Written by A how To Company Contributor

How Hard Inquiries and Soft Inquiries Work

Credit inquiries can be confusing because not every credit check affects your score the same way.

Some credit checks may lower your score slightly. Others have no scoring impact at all.

That is why understanding the difference between hard inquiries and soft inquiries matters before you apply for credit, shop for loans, or check your own score.

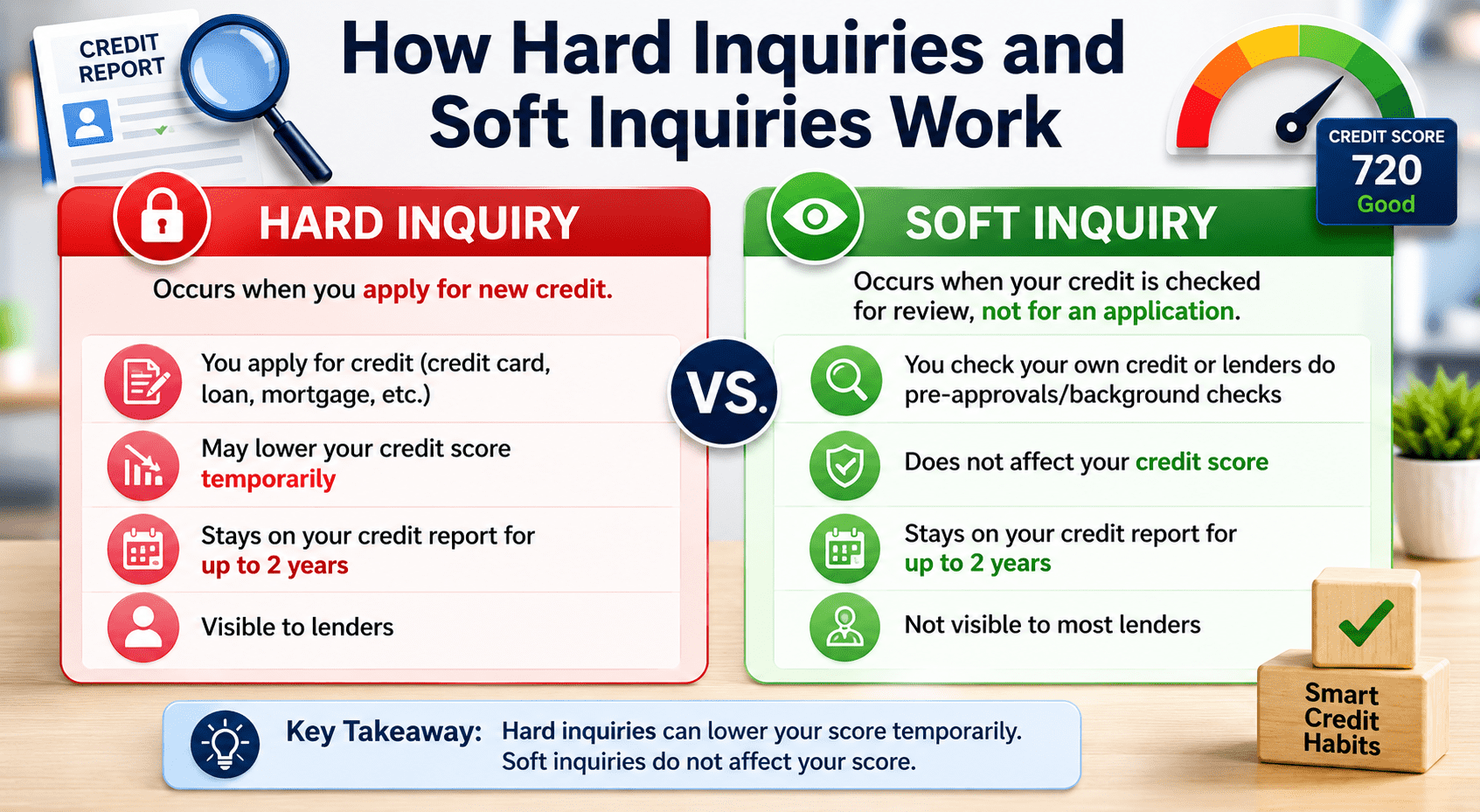

Hard inquiries and soft inquiries both involve credit checks, but they affect credit scores differently.

Quick Answer

The difference may sound small, but it can matter when you are preparing for a mortgage, auto loan, credit card application, or apartment approval.

What Is a Credit Inquiry?

A credit inquiry happens when someone checks information in your credit file.

According to the Consumer Financial Protection Bureau, credit inquiries are generally divided into two categories: hard inquiries and soft inquiries.

Both involve someone accessing credit information, but they are treated differently by credit scoring systems.

Key Takeaway

The main difference is purpose. Hard inquiries are usually tied to applications for new credit. Soft inquiries are usually tied to credit monitoring, preapprovals, or account reviews.

What Is a Hard Inquiry?

A hard inquiry usually happens when you apply for new credit and the lender checks your credit report to decide whether to approve you.

Common examples include applying for:

- A credit card

- A mortgage

- An auto loan

- A personal loan

- A student loan

- A line of credit

What Is a Soft Inquiry?

A soft inquiry is a credit check that does not affect your credit score.

Soft inquiries commonly happen when:

- You check your own credit score

- You check your own credit report

- A company reviews your credit for a preapproval offer

- An existing lender reviews your account

- An employer checks credit information where legally allowed

The CFPB states that soft inquiries do not affect your credit score. The agency also notes that when an existing lender pulls your credit, it is generally a soft inquiry and does not affect your score.

You can read more from the Consumer Financial Protection Bureau.

How Much Do Hard Inquiries Affect Your Credit Score?

A hard inquiry usually has a small and temporary impact, but the exact effect depends on your overall credit profile.

Someone with a long, strong credit history may see little movement. Someone with a short credit history or many recent applications may be affected more.

According to Experian, hard inquiries can stay on a credit report for up to two years, though their scoring impact is often much shorter.

Important Detail

A single hard inquiry is usually not a major problem. Several hard inquiries in a short period may create more concern because they can suggest higher borrowing risk.

This is why applying for multiple credit cards or loans without a clear plan can cause unnecessary score damage.

How Rate Shopping Works

There is one important exception people should understand.

Credit scoring models often treat multiple inquiries for certain loan types as one inquiry when they happen within a short shopping window.

This is designed to let consumers compare rates without being punished for shopping around.

Rate shopping commonly applies to:

- Mortgage loans

- Auto loans

- Student loans

According to myFICO, newer FICO models may treat certain rate shopping inquiries within a 45 day window as one inquiry, while older FICO versions may use a 14 day window.

Usually no. Rate shopping protections are commonly associated with mortgages, auto loans, and student loans. Multiple credit card applications may be treated as separate hard inquiries.

What If You See an Inquiry You Do Not Recognize?

An unfamiliar hard inquiry should not be ignored.

Sometimes it may come from a lender using a name you do not recognize. Other times it may suggest identity theft or an unauthorized credit application.

If you see an inquiry you do not recognize, consider these steps:

- Check whether the company has another business name

- Review recent applications you submitted

- Check all three credit reports

- Contact the lender listed on the inquiry

- Dispute inaccurate information if needed

- Consider a fraud alert or credit freeze if identity theft is suspected

The Federal Trade Commission recommends reviewing credit reports for mistakes and signs of identity theft.

Consumers can access free credit reports through AnnualCreditReport.com, the federally authorized source for free credit reports.

When to Pay Attention

Final Thoughts

Hard inquiries and soft inquiries both involve credit checks, but they do not affect your credit in the same way.

Hard inquiries are usually connected to applications for new credit and may temporarily lower your score. Soft inquiries happen during credit monitoring, preapprovals, account reviews, or when you check your own credit, and they do not affect your score.

The goal is not to fear every inquiry. The goal is to understand when an inquiry matters and when it does not.

A few well planned hard inquiries are usually manageable. Repeated applications without a strategy can create unnecessary credit damage.