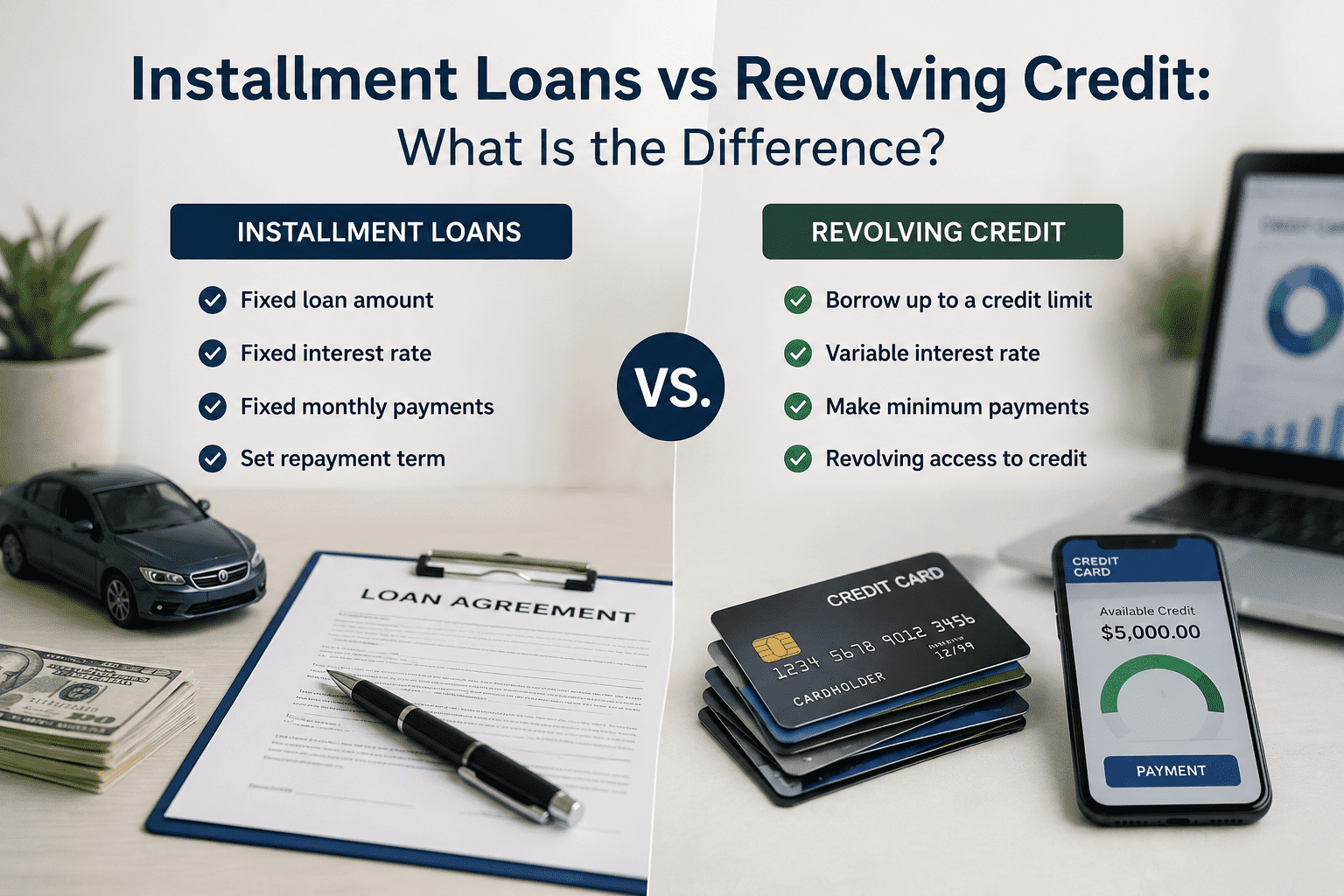

Installment Loans vs Revolving Credit: What Is the Difference?

Written by A how To Company Contributor

Installment Loans vs Revolving Credit: What Is the Difference?

Not all credit accounts work the same way.

A credit card, auto loan, mortgage, personal loan, and student loan may all appear on a credit report, but they are not treated exactly the same.

Some accounts let you borrow, repay, and borrow again. Others give you one loan amount that you pay back over time.

That difference matters because lenders and credit scoring models often look at the types of accounts you manage.

Installment loans and revolving credit are two major types of credit accounts that work in very different ways.

Quick Answer

Revolving credit lets you borrow repeatedly up to a credit limit, repay the balance, and borrow again. Credit cards are the most common example. Installment loans give you a fixed loan amount that you repay through scheduled payments over time. Auto loans, mortgages, personal loans, and student loans are common installment loans.

Understanding these account types can help you make better borrowing decisions and understand why a healthy mix of credit may help your score over time.

Why Different Account Types Matter

Credit reports do more than show whether you pay on time.

They also show what types of credit you have managed.

A lender may want to know whether you have experience handling:

- Credit cards

- Auto loans

- Mortgages

- Personal loans

- Student loans

Key Takeaway

According to myFICO, credit mix can include credit cards, retail accounts, installment loans, finance company accounts, and mortgage loans.

What Is Revolving Credit?

Revolving credit gives you access to a credit limit that you can use repeatedly.

You can borrow money, pay it back, and borrow again as long as the account remains open and in good standing.

Revolving credit does not have one fixed payoff schedule. Your balance can rise or fall depending on how much you spend and repay.

The most common example is a credit card.

If your card has a $5,000 credit limit, you can charge purchases up to that limit. When you pay down the balance, available credit becomes usable again.

Credit card balances are compared with credit limits to calculate credit utilization. High utilization can hurt credit scores, while lower utilization is generally better.

The Consumer Financial Protection Bureau explains that credit utilization compares the amount of credit you are using with your total available credit.

What Is an Installment Loan?

An installment loan is a loan for a set amount of money that you repay over a scheduled period of time.

Unlike revolving credit, you usually cannot keep borrowing from the same loan after you pay it down.

An installment loan usually has a fixed loan amount, a repayment term, and scheduled payments.

Installment loans are often used for specific purchases or major financial needs.

Examples include auto loans, mortgages, personal loans, and student loans.

Common Examples of Each Account Type

A simple way to understand the difference is to look at common account examples.

Credit Cards

Credit cards are revolving accounts. You have a credit limit, and your balance changes depending on spending and payments.

Credit cards can be powerful tools when managed well, but high balances can hurt scores quickly because of credit utilization.

Auto Loans

Auto loans are installment loans. You borrow money to purchase a vehicle and repay the loan through scheduled payments.

Once the loan is paid off, the account is usually closed.

Mortgages

Mortgages are installment loans used to finance real estate.

Because mortgages are large and long term, lenders pay close attention to payment history and overall credit profile when approving borrowers.

Personal Loans

Personal loans are usually installment loans. They may be used for debt consolidation, major expenses, emergencies, or other approved purposes.

They often have fixed monthly payments over a set term.

Student Loans

Student loans are also installment loans. They are used to finance education costs and are repaid over time according to the loan terms.

Simple Rule

Credit cards are usually revolving credit. Auto loans, mortgages, personal loans, and student loans are usually installment loans.

How These Accounts Affect Credit Scores

Both revolving credit and installment loans can help or hurt your credit depending on how they are managed.

Credit scoring models often consider:

- Whether payments are made on time

- How much debt is owed

- How long accounts have been open

- How recently new accounts were opened

- The mix of account types

According to myFICO, credit mix makes up 10 percent of a FICO Score, although payment history and amounts owed are larger factors.

Why a Healthy Credit Mix Can Help Over Time

A healthy credit mix shows that you can manage different kinds of credit responsibly.

For example, someone with a long history of managing both a credit card and an auto loan responsibly may appear more experienced than someone with only one very new account.

However, credit mix is not the most important scoring factor.

Payment history and amounts owed usually matter much more.

Important Detail

A healthy credit mix can help scores over time, but it should develop naturally through responsible borrowing rather than unnecessary debt.

myFICO notes that having a mix of installment and revolving loans can play a part in your score, but credit mix alone is unlikely to determine whether you qualify for credit.

Final Thoughts

Installment loans and revolving credit are both important parts of the credit system, but they work differently.

Revolving credit, such as credit cards, gives ongoing access to a credit limit. Installment loans, such as auto loans, mortgages, personal loans, and student loans, are repaid over a set schedule.

A healthy mix of account types can help your credit profile over time, but it should never come at the cost of taking on debt you do not need.

The best credit mix is one you can manage responsibly, pay on time, and keep under control.