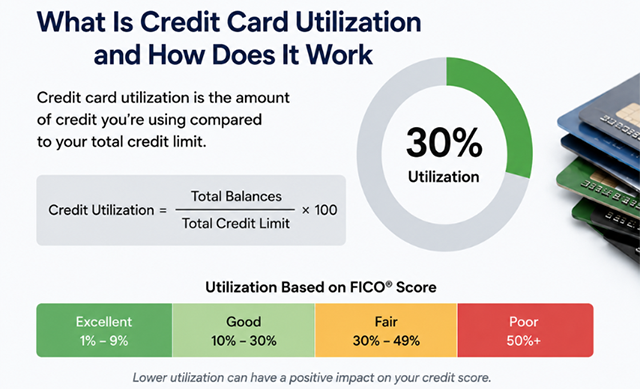

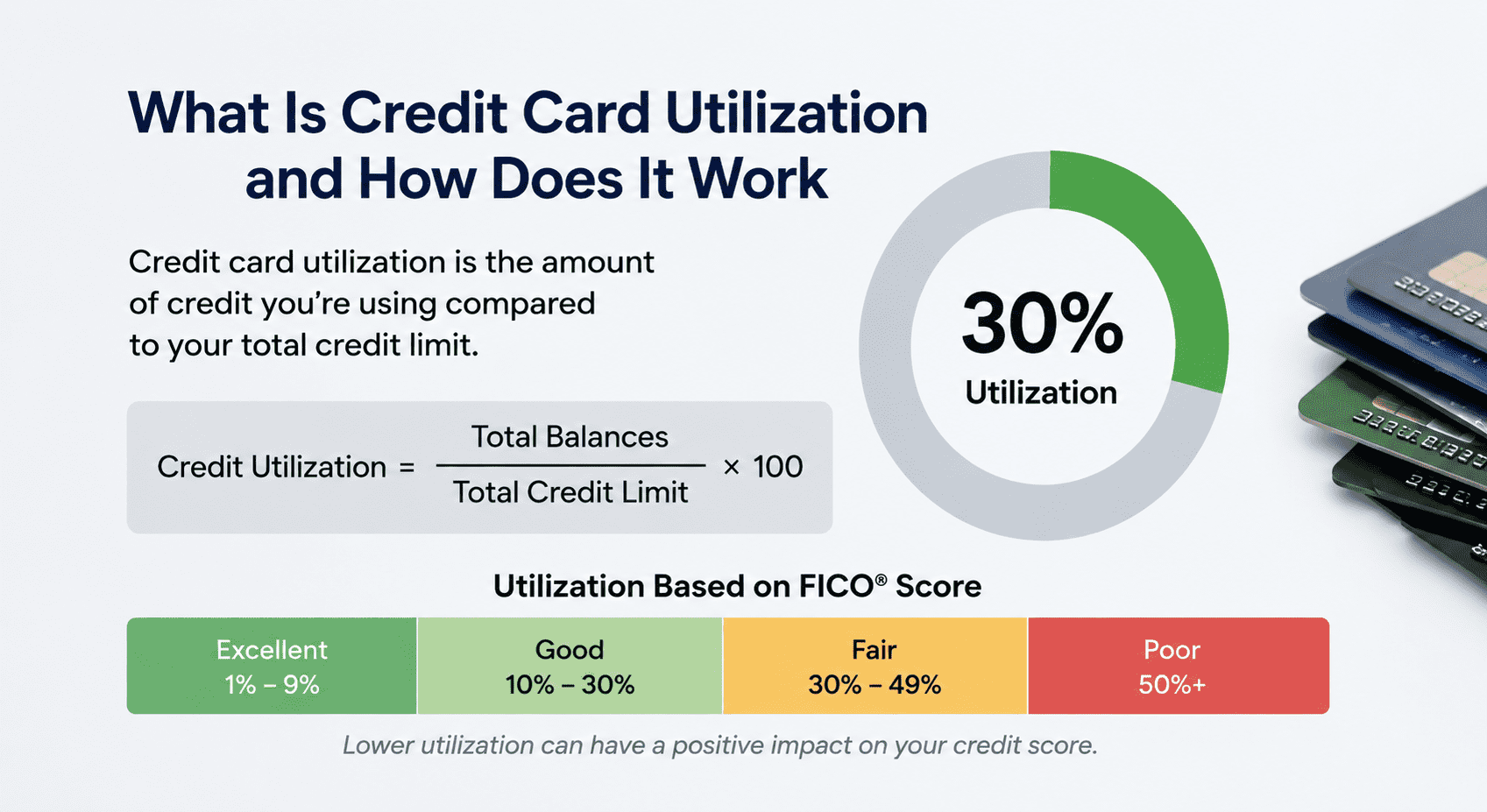

What Is Credit Card Utilization and How Does It Work?

Written by A how To Company Contributor

What Is Credit Card Utilization and How Does It Work?

Many people hear the term “credit card utilization” while trying to improve their credit score, but very few fully understand how important it actually is.

In reality, credit utilization is one of the most powerful factors affecting many credit scores. In some situations, it can be the difference between a good score and a poor one.

Credit utilization measures how much of your available credit you are currently using.

Quick Answer

Credit card utilization is the percentage of your available credit that you are currently using. Lower utilization generally helps credit scores, while high utilization can negatively affect them.

What surprises many people is how quickly utilization can affect a credit score. Unlike some credit factors that take years to improve, utilization can sometimes change your score within one billing cycle.

That is why understanding how it works is so important.

What Is Credit Card Utilization?

Credit utilization compares your current credit card balances to your total available credit limits.

In simple terms, it answers this question:

How much of your available credit are you using right now?

That percentage matters because lenders and scoring models may view high utilization as a sign of increased financial risk.

According to the Consumer Financial Protection Bureau, credit utilization is an important part of many credit scoring systems.

Why Credit Utilization Matters So Much

Many people focus entirely on payment history while ignoring utilization.

That can be a major mistake.

You can make every payment on time and still see your score suffer if your balances remain too high compared with your limits.

Key Takeaway

High balances can hurt your score even if you never miss a payment.

This is one reason why people sometimes see sudden score drops after large purchases, even when they plan to pay the balance off later.

The credit bureaus only see the balance that gets reported.

What Is a Good Credit Utilization Percentage?

Most financial experts recommend keeping utilization below 30 percent.

However, people with the strongest credit scores often stay below 10 percent.

- Above 50 percent may significantly hurt your score

- Below 30 percent is usually much better

- Below 10 percent is often viewed most favorably

How Credit Utilization Is Calculated

There are actually two types of utilization that can matter:

- Individual card utilization

- Total overall utilization

Individual Card Utilization

This measures utilization on each specific card.

For example:

- Card 1 limit: $1,000

- Card 1 balance: $900

- Card 1 utilization: 90 percent

Even if your total utilization is decent, one maxed out card can still negatively affect your score.

Total Utilization

This measures all balances combined compared with all available credit combined.

Example:

- Total credit limits: $10,000

- Total balances: $2,000

- Total utilization: 20 percent

Common Credit Utilization Mistakes

How to Improve Credit Utilization Quickly

If your utilization is high, several strategies may help relatively quickly.

- Pay down balances aggressively

- Make multiple payments during the month

- Request higher credit limits

- Spread balances across cards more evenly

- Avoid large purchases before statement closing dates

One of the Fastest Credit Score Improvements

Lowering utilization is often one of the fastest legitimate ways to improve a credit score because updated balances may report monthly.

According to Experian, keeping balances low relative to available credit may positively affect credit scores.

Final Thoughts

Credit card utilization is one of the most misunderstood parts of credit scoring, but it is also one of the most important.

Many people focus only on making payments while overlooking how much of their available credit they are using.

The good news is that utilization is also one of the few factors that can sometimes improve relatively quickly.

Understanding utilization can help you make smarter credit decisions and improve your score much faster than many people realize.