How to Improve Your Credit Score Quickly: What Actually Works and What Does Not

Written by A how To Company Contributor

How to Improve Your Credit Score Quickly: What Actually Works and What Does Not

If you are trying to improve your credit score quickly, you are probably dealing with a real financial goal.

Maybe you want to buy a car. Maybe you are preparing to apply for a mortgage. Maybe you are tired of getting denied for credit cards or stuck paying high interest rates.

A strong credit score can affect loan approvals, interest rates, rental applications, and financial flexibility.

Quick Answer

The fastest legitimate way to improve your credit score is usually to lower your credit card utilization, catch up missed payments, correct credit report errors, and avoid new hard inquiries while your updated balances report to the credit bureaus.

If you are trying to improve your credit score quickly, you are probably dealing with a real financial goal.

Maybe you want to buy a car. Maybe you are preparing to apply for a mortgage. Maybe you are tired of getting denied for credit cards or stuck paying high interest rates.

The Fastest Legitimate Way to Improve a Credit Score

For many people, the quickest improvement comes from lowering credit card utilization.

Credit utilization means how much of your available revolving credit you are using. If your credit card has a $5,000 limit and you owe $4,000, your utilization is 80 percent.

That is high. Even if you pay on time every month, a high balance compared with your credit limit can still hurt your score.

According to the Consumer Financial Protection Bureau, credit utilization can affect your credit score because lenders may see high usage as a sign of increased financial risk.

Key Takeaway

If your credit cards are close to their limits, paying them down may help your score faster than many other strategies.

What Utilization Percentage Should You Aim For?

Many experts recommend keeping credit utilization below 30 percent. However, people with the highest credit scores often keep utilization below 10 percent.

- Above 50 percent may significantly hurt your score.

- Below 30 percent is usually better.

- Below 10 percent is often ideal.

This is why paying down one heavily used credit card can sometimes create a noticeable improvement once the new balance is reported.

Credit card issuers usually report balances to the credit bureaus about once per month. That means a lower balance can appear on your report relatively quickly compared with older negative marks, which may remain for years.

The Reality Most Articles Do Not Mention

You should be careful with any article that promises an instant credit score transformation.

Credit scores are designed to reward responsible behavior over time. Late payments, collections, repossessions, and bankruptcies do not disappear overnight.

According to Experian, most negative information can stay on a credit report for seven years, while some bankruptcies can remain for up to ten years.

That does not mean you are stuck. It simply means you need to separate quick wins from long term repair.

Important Reality Check

Fast credit improvement usually means weeks to months, not overnight. The fastest results often come from fixing the parts of your report that update the soonest.

The Most Effective Ways to Improve Credit Quickly

If your goal is a faster score improvement, credit card balances often deserve priority.

Focus first on maxed out cards, cards above 50 percent utilization, and cards close to their limits. Lowering those balances may have a stronger short term impact than paying extra on installment loans.

If your lender increases your credit limit while your balance stays the same, your utilization percentage drops.

For example, a $2,000 balance on a $2,500 limit equals 80 percent utilization. The same $2,000 balance on a $10,000 limit equals 20 percent utilization.

Before requesting an increase, ask whether the lender uses a soft inquiry or a hard inquiry.

If someone with excellent credit adds you as an authorized user on a well managed account, it may help some scoring models.

This works best when the account has a long history, low utilization, and perfect payment history.

It can backfire if the primary user carries high balances or misses payments.

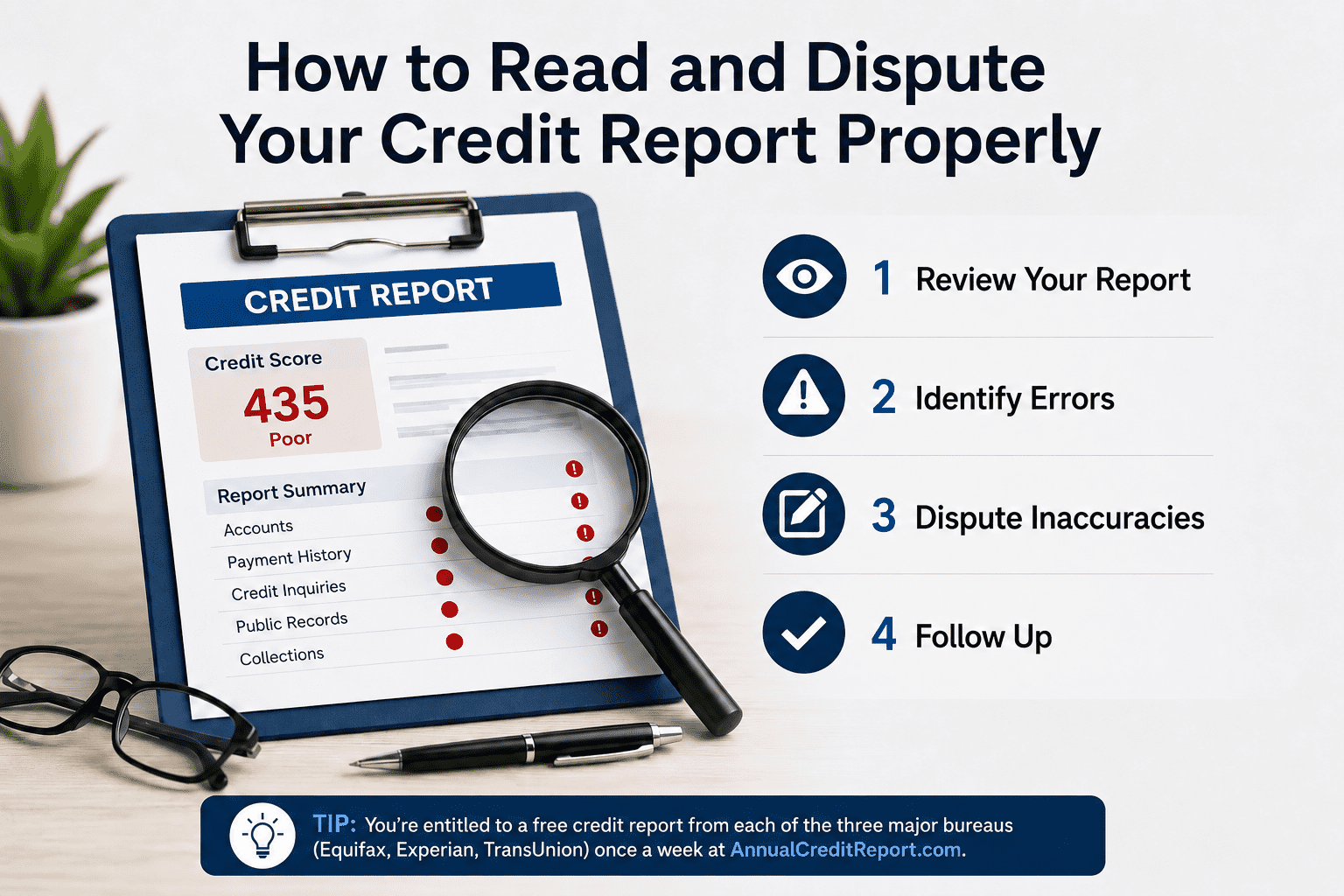

Credit report errors can include incorrect late payments, duplicate accounts, inaccurate balances, identity mistakes, and fraudulent accounts.

A Federal Trade Commission report found that some consumers identified errors on their credit reports.

You can review your reports through AnnualCreditReport.com, which is the federally authorized source for free credit reports.

Payment history is one of the most important credit score factors.

If you are behind, catching up quickly matters. Set up automatic minimum payments so a simple oversight does not create another negative mark.

Closing a card can reduce your available credit and raise your utilization percentage.

If the card has no annual fee and does not tempt you to overspend, keeping it open may help preserve available credit and account history.

Applying for several accounts in a short period can create hard inquiries and may make lenders view you as a higher risk applicant.

Strategic applications are usually better than applying everywhere and hoping one approval works.

How Fast Can a Credit Score Actually Improve?

The timeline depends on what is hurting your score.

If your main issue is high utilization, you may see movement after your lower balances are reported. That can sometimes happen within one or two billing cycles.

If your score is being held down by late payments, collections, or other serious negative marks, the process usually takes longer.

That is not failure. That is simply how credit scoring works.

A Practical Fast Improvement Plan

If you want the highest chance of improving your score as quickly as realistically possible, follow this order.

- Pay down credit card balances aggressively.

- Bring utilization below 30 percent, then below 10 percent if possible.

- Catch up any missed payments immediately.

- Review your credit reports carefully for errors.

- Dispute inaccurate information with the credit bureaus.

- Avoid unnecessary hard inquiries.

- Keep older positive accounts open when appropriate.

- Give updated balances time to report.

The Biggest Mistake to Avoid

Final Thoughts

Improving your credit score quickly is possible, but realistic expectations matter.

In the credit world, fast usually means weeks to months. The good news is that some of the strongest improvements come from actions you can control.

Lower your utilization. Make payments consistently. Correct errors. Avoid new damage. Then give the system time to update.

The people who improve their scores the fastest are usually not using secret tricks. They are focusing on the factors that matter most.