What Are Credit Bureaus and How Do They Work?

Written by A how To Company Contributor

What Are Credit Bureaus and How Do They Work?

Most people hear about credit bureaus when checking their credit score, applying for a loan, or dealing with a credit problem.

However, many people do not fully understand what credit bureaus actually are, why they exist, or how much influence they have over everyday financial decisions.

In reality, credit bureaus play a massive role in the modern financial system.

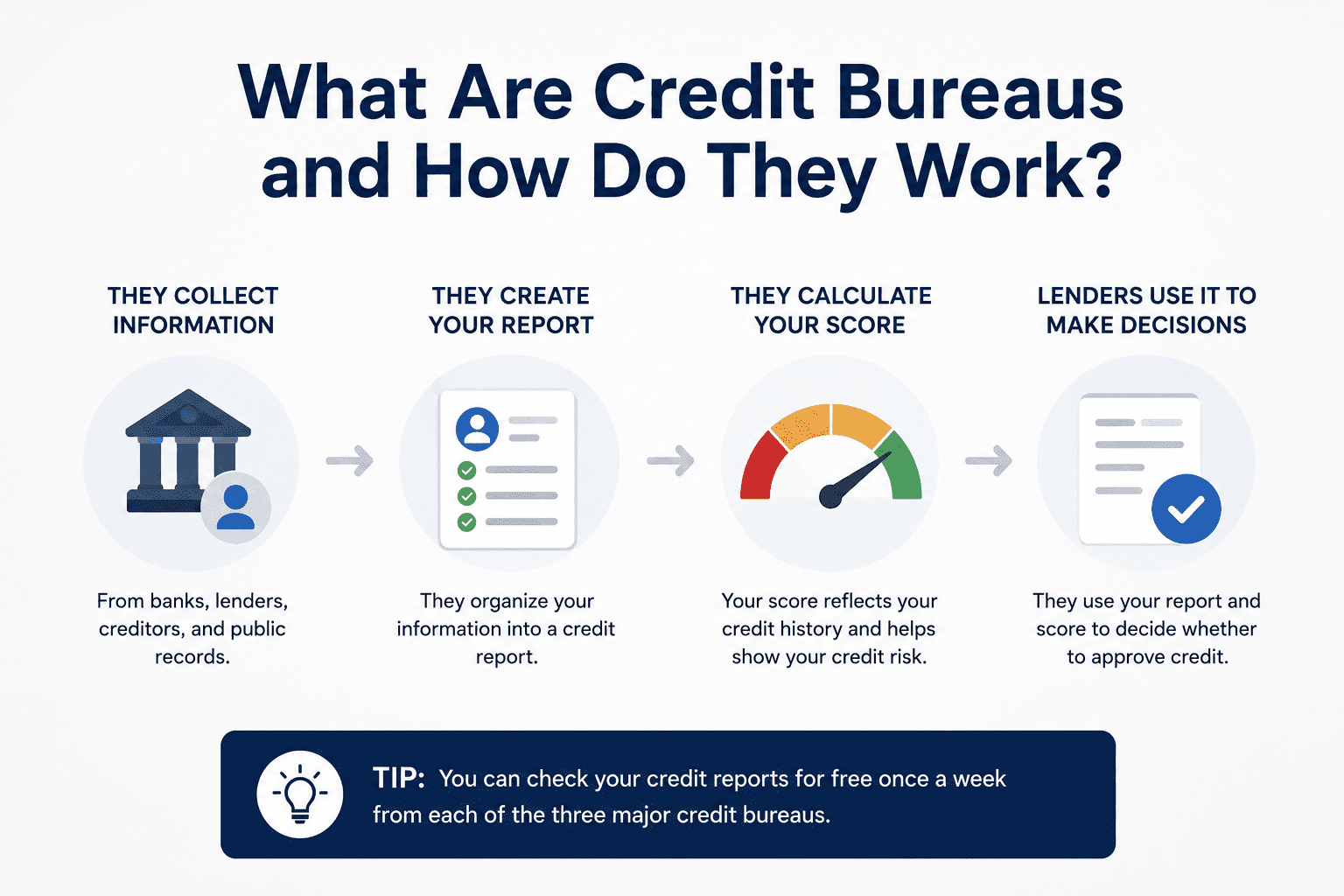

Credit bureaus collect and organize financial data that lenders use to evaluate borrowing risk.

Quick Answer

Credit bureaus are companies that collect, organize, and maintain financial information about consumers. Lenders use this information to help evaluate credit risk when people apply for loans, credit cards, mortgages, apartments, and sometimes even jobs.

While most people know the names Experian, Equifax, and TransUnion, fewer people understand how these companies actually gather information and why credit reports from each bureau may not always match.

What Are Credit Bureaus?

Credit bureaus are private companies that track and maintain consumer credit information.

Their primary job is to collect financial data from lenders and organize it into credit reports.

These reports may include:

- Credit card accounts

- Loan balances

- Payment history

- Collections

- Bankruptcies

- Credit inquiries

- Available credit limits

Key Takeaway

Credit bureaus do not decide whether you are approved for a loan. Instead, they provide information that lenders use to make those decisions.

In other words, they act as large financial information databases.

Why Were Credit Bureaus Created?

Before modern credit reporting systems existed, lenders had a major problem.

They had very limited ways to evaluate whether someone was likely to repay borrowed money.

Early lending decisions often relied on:

- Personal relationships

- Local reputation

- Word of mouth

- Community knowledge

As the economy grew and lending expanded nationally, this system became impractical.

Credit bureaus emerged to create standardized systems for tracking borrowing behavior and repayment history.

Over time, credit reporting became central to the financial system because lenders wanted faster and more consistent ways to evaluate risk.

The Three Major Credit Bureaus

In the United States, the three major consumer credit bureaus are:

Although these companies perform similar functions, their reports may not always contain identical information.

How Credit Bureaus Actually Work

Credit bureaus receive information from lenders, banks, credit card companies, collection agencies, and other financial institutions.

These companies regularly report information such as:

- Account balances

- Payment history

- Credit limits

- Missed payments

- Account openings

- Account closures

The bureaus then organize this information into credit reports.

Lenders may review those reports when evaluating applications for:

- Credit cards

- Mortgages

- Auto loans

- Personal loans

- Apartment rentals

Important Detail

Why Your Credit Scores May Be Different

Many people are surprised when they discover they do not have one single universal credit score.

Instead, scores may vary depending on:

- Which bureau supplied the data

- Which scoring model was used

- When the information was updated

How Credit Bureaus Affect Everyday Life

Credit bureau information affects far more than just loan approvals.

Your credit reports and scores may influence:

- Interest rates

- Credit card approvals

- Mortgage qualification

- Apartment applications

- Insurance pricing in some states

- Utility account approvals

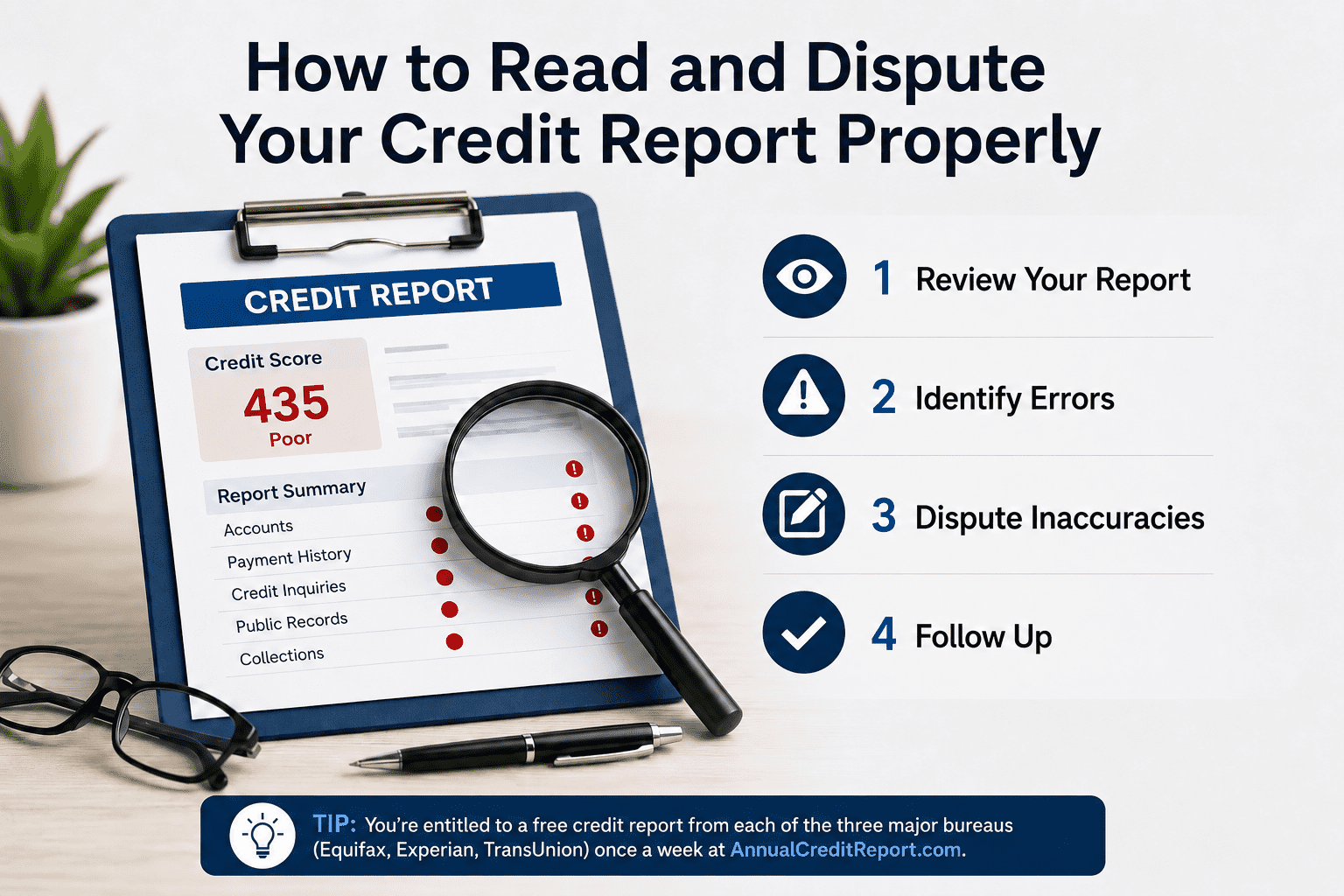

Because these reports affect so many financial decisions, accuracy matters enormously.

According to the Federal Trade Commission, consumers should regularly review their credit reports for potential inaccuracies or fraudulent activity.

Consumers can access free credit reports through AnnualCreditReport.com, the federally authorized source for free annual credit reports.

Final Thoughts

Credit bureaus play a central role in the modern financial system because they help lenders evaluate borrowing risk quickly and consistently.

While many people think of credit bureaus as mysterious companies controlling credit scores, their primary role is collecting and organizing financial information.

Understanding how these companies work can help you better manage your credit profile, monitor your reports, and catch potential problems early.

The more you understand how credit reporting works, the easier it becomes to make smarter financial decisions and protect your financial future.