Why Your Mortgage Credit Score May Be Different From the Score in Your App

Written by A how To Company Contributor

Why Your Mortgage Credit Score May Be Different From the Score in Your App

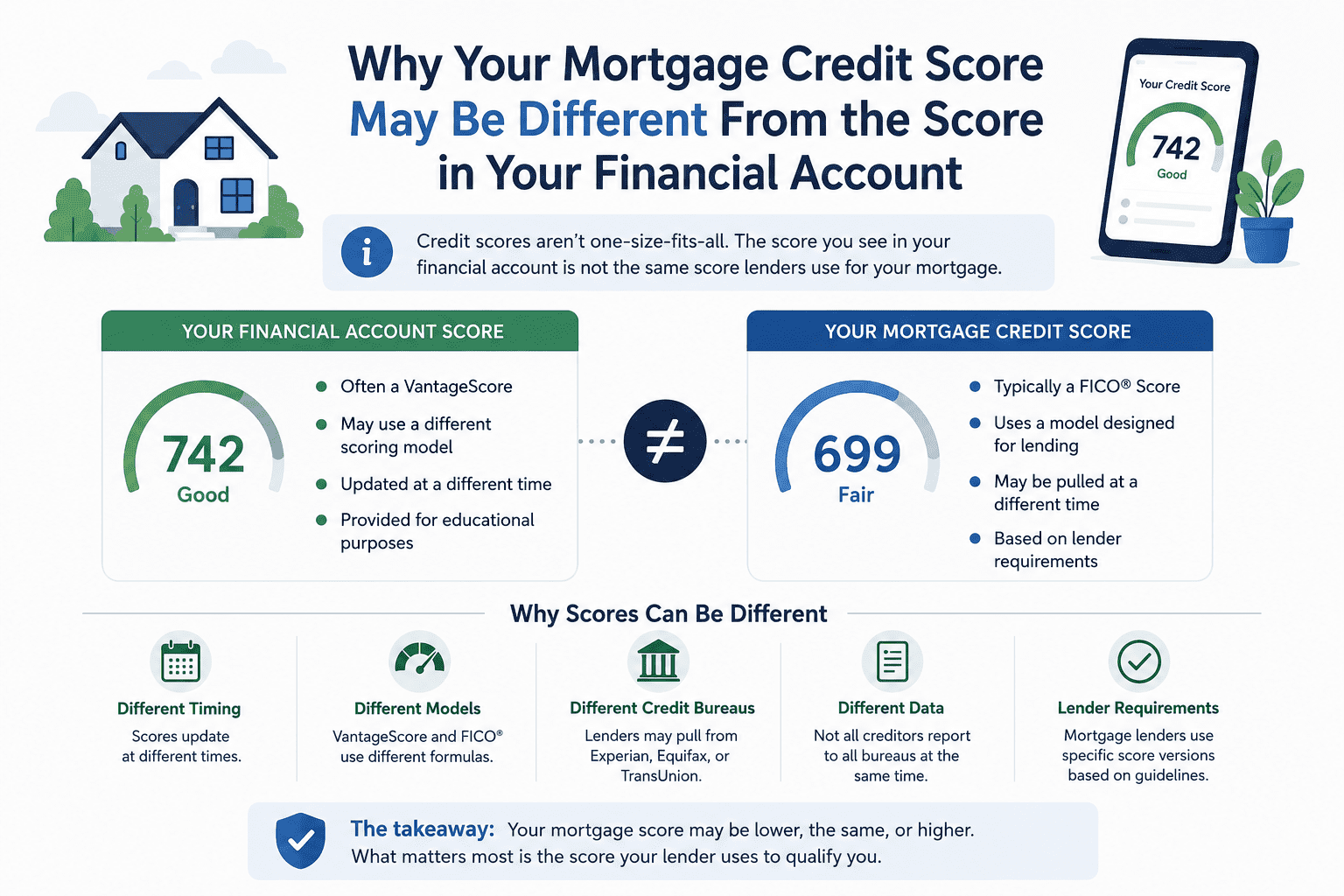

One of the most confusing moments during the mortgage process happens when someone checks their credit score in an app and sees a strong number, only to discover the lender is using a completely different score.

Many people assume they have one official credit score. In reality, that is not how credit scoring works.

Mortgage lenders often use different scoring models than the scores shown in free apps and websites.

Mortgage lenders often use different credit scoring models than the scores shown in consumer apps.

Quick Answer

This is why someone may see a 740 score in a credit monitoring app but receive a lower score from a mortgage lender.

Why Credit Scores Can Be Different

Many people are surprised to learn they do not have one single universal credit score.

Instead, people may have:

- Multiple FICO Scores

- Multiple VantageScores

- Industry specific scores

- Scores from different bureaus

Key Takeaway

Different lenders may use completely different scoring models depending on the type of loan being evaluated.

What Mortgage Lenders Usually Use

Mortgage lenders commonly use older FICO scoring models developed specifically for mortgage lending decisions.

These models are often:

- FICO Score 2 from Experian

- FICO Score 5 from Equifax

- FICO Score 4 from TransUnion

These versions may weigh certain behaviors differently than newer scoring models.

- Often older FICO models

- Designed specifically for mortgage risk

- Pulled from all three major bureaus

- May react differently to utilization and late payments

According to myFICO, lenders may use different FICO score versions depending on the type of credit application.

What Many Apps and Websites Show

Many free credit monitoring apps display educational scores or VantageScores rather than the mortgage specific scores lenders often use.

These scores are still legitimate credit scores, but they may not be the same versions used during a mortgage application.

- Often VantageScores

- Sometimes newer FICO versions

- Designed for general monitoring

- May differ significantly from mortgage scores

This does not mean the app is inaccurate. It simply means the scoring model is different.

Different FICO Models Can Produce Different Numbers

Even within the FICO system itself, there are multiple scoring versions.

Some models are designed specifically for:

- Credit cards

- Auto loans

- Mortgages

- General lending

Because these models evaluate risk differently, the scores may vary.

Important Detail

A person may legitimately have several different FICO Scores at the same time depending on the model being used.

What Mortgage Lenders Often Focus On

Mortgage lenders commonly pull reports from all three major credit bureaus:

- Experian

- Equifax

- TransUnion

Then, instead of averaging all three scores, many lenders use the middle score.

Example:

- Experian: 742

- Equifax: 718

- TransUnion: 730

In this example, the lender may focus primarily on the 730 middle score.

In many situations, lenders may use the lower middle score between the two applicants when evaluating mortgage eligibility.

Why This Difference Matters

Understanding this difference helps people avoid panic during the mortgage process.

Many borrowers incorrectly assume:

“The lender made a mistake because my app showed a higher score.”

Usually, the lender is simply using a different scoring model.

This also explains why mortgage preparation often involves focusing heavily on:

- Credit utilization

- Payment history

- Avoiding new inquiries

- Reducing balances before applying

Mortgage Preparation Tip

People planning to buy a home should avoid opening unnecessary accounts or making major credit changes shortly before applying for a mortgage.

Final Thoughts

Mortgage credit scores often differ from app based scores because lenders frequently use specialized mortgage focused FICO models rather than the educational scores many consumers see online.

This does not necessarily mean one score is wrong.

It simply means different scoring systems are being used for different purposes.

Understanding how these models work can help reduce confusion and better prepare borrowers for the mortgage process.

The most important thing is not obsessing over one exact number, but building strong long term credit habits that improve scores across all models.

1- AI for writing (content creation)

Lorem Ipsumu00a0is simply dummy text of the printing and typesetting industry. Lorem Ipsum has been the industry’s standard dummy text ever since the 1500s, when an unknown printer took a galley of type and scrambled it to make a type specimen book. It has survived not only five centuries, but also the leap into electronic typesetting, remaining essentially unchanged. It was popularised in the 1960s with the release of Letraset sheets containing Lorem Ipsum passages, and more recently with desktop publishing software like Aldus PageMaker including versions of Lorem Ipsum. Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur. Excepteur sint occaecat cupidatat non proident, sunt in culpa qui officia deserunt mollit anim id est laborum.2-TAI for design (logos, social media)

Lorem Ipsumu00a0is simply dummy text of the printing and typesetting industry. Lorem Ipsum has been the industry’s standard dummy text ever since the 1500s, when an unknown printer took a galley of type and scrambled it to make a type specimen book. It has survived not only five centuries, but also the leap into electronic typesetting, remaining essentially unchanged. It was popularised in the 1960s with the release of Letraset sheets containing Lorem Ipsum passages, and more recently with desktop publishing software like Aldus PageMaker including versions of Lorem Ipsum.

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur. Excepteur sint occaecat cupidatat non proident, sunt in culpa qui officia deserunt mollit anim id est laborum.

3- AI for productivity & automation

Lorem Ipsumu00a0is simply dummy text of the printing and typesetting industry. Lorem Ipsum has been the industry’s standard dummy text ever since the 1500s, when an unknown printer took a galley of type and scrambled it to make a type specimen book. It has survived not only five centuries, but also the leap into electronic typesetting, remaining essentially unchanged. It was popularised in the 1960s with the release of Letraset sheets containing Lorem Ipsum passages, and more recently with desktop publishing software like Aldus PageMaker including versions of Lorem Ipsum.

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur. Excepteur sint occaecat cupidatat non proident, sunt in culpa qui officia deserunt mollit anim id est laborum.

4-Free vs paid tools comparison

Lorem Ipsumu00a0is simply dummy text of the printing and typesetting industry. Lorem Ipsum has been the industry’s standard dummy text ever since the 1500s, when an unknown printer took a galley of type and scrambled it to make a type specimen book. It has survived not only five centuries, but also the leap into electronic typesetting, remaining essentially unchanged. It was popularised in the 1960s with the release of Letraset sheets containing Lorem Ipsum passages, and more recently with desktop publishing software like Aldus PageMaker including versions of Lorem Ipsum.

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur. Excepteur sint occaecat cupidatat non proident, sunt in culpa qui officia deserunt mollit anim id est laborum.

5- How to use AI to earn money

Lorem Ipsumu00a0is simply dummy text of the printing and typesetting industry. Lorem Ipsum has been the industry’s standard dummy text ever since the 1500s, when an unknown printer took a galley of type and scrambled it to make a type specimen book. It has survived not only five centuries, but also the leap into electronic typesetting, remaining essentially unchanged. It was popularised in the 1960s with the release of Letraset sheets containing Lorem Ipsum passages, and more recently with desktop publishing software like Aldus PageMaker including versions of Lorem Ipsum.

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur. Excepteur sint occaecat cupidatat non proident, sunt in culpa qui officia deserunt mollit anim id est laborum.